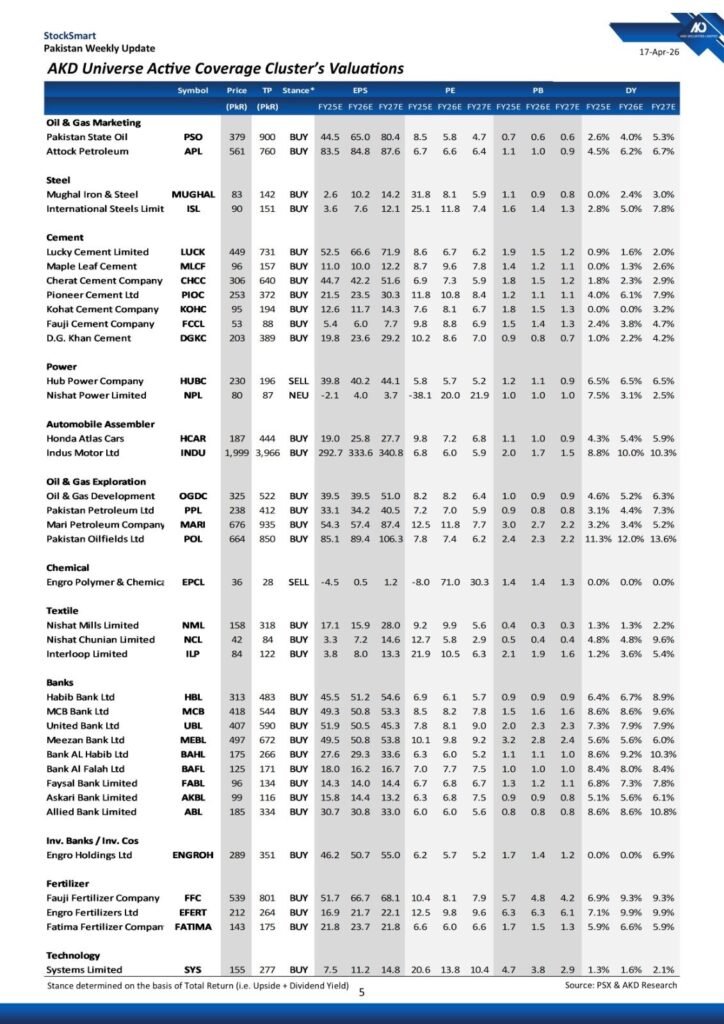

AKD Securities maintains bullish outlook on key sectors as valuations remain attractive despite recent market volatility.

Key Takeaways

• Major commercial banks including BAHL and MCB offer dividend yields exceeding 8 percent while maintaining attractive price-to-book ratios.

• Oil and gas exploration firms like POL and PPL show massive upside potential with target prices significantly higher than current market levels.

• The cement sector remains a buy across the board with Lucky Cement and DGKC expected to see price-to-earnings ratios improve through FY2027.

Karachi, Pakistan – The latest AKD Universe Active Coverage Cluster report reveals a dominant “BUY” stance across major industrial and financial sectors. While the Hub Power Company (HUBC) and Engro Polymer & Chemicals (EPCL) carry “SELL” ratings, the broader market shows significant upside potential based on Total Return metrics. Within the energy sector, Pakistan State Oil (PSO) stands out with a target price of 900 PkR against a current price of 379 PkR, suggesting a robust recovery path.

Pakistan State Oil shows the highest upside potential in the marketing sector with a target price nearly three times its current valuation.

Sectoral Valuations and Dividend Yields

The banking sector continues to offer high dividend yields, with Bank AL Habib (BAHL) and Allied Bank (ABL) both yielding above 10% for FY26E. In the exploration space, Pakistan Oilfields Ltd (POL) remains a standout for income seekers, boasting a projected dividend yield of 12.0% for FY26E. Technology giant Systems Limited (SYS) also shows a strong growth trajectory with a target price of 277 PkR, nearly double its current market value.

Energy Sector: Marketing and Exploration Synergies

The energy chain presents perhaps the most dramatic valuation gap. Within the Oil and Gas Marketing space, Pakistan State Oil (PSO) remains a focal point for recovery. While the current price hovers around 379 PkR, the target price of 900 PkR suggests that the market has yet to price in the long-term resolution of circular debt and operational efficiencies. Attock Petroleum (APL) follows a similar trajectory with a 760 PkR target, supported by a healthy 6.2% dividend yield projection for FY26E.

In the Exploration and Production (E&P) sector, the data points to a “cash cow” environment. Pakistan Oilfields Ltd (POL) is currently trading at 664 PkR but carries a target of 850 PkR. More importantly for income-focused portfolios, POL offers a projected dividend yield of 12.0% for FY26E, rising to 13.6% by FY27E. Mari Petroleum and PPL similarly show robust upside, with PPL’s target price of 412 PkR representing nearly double its current market value. These valuations reflect a sector that is fundamentally undervalued relative to its dollar-indexed revenue streams and global energy price trends.

Financials: The Dividend Powerhouse

The banking sector remains the bedrock of the KSE-100’s yield profile. Commercial banks are currently trading at price-to-book (PB) ratios that are historically attractive, often below 1.0x. For instance, Habib Bank Ltd (HBL) and Allied Bank (ABL) are trading at PB ratios of 0.9 and 0.8 respectively for FY25E. This suggests that the market is valuing these institutions at less than their liquidated net worth, despite consistent profitability.

Dividend yields in the banking cluster are particularly aggressive. Bank AL Habib (BAHL) and MCB Bank are projected to deliver yields of 9.2% and 8.6% respectively in FY26E. As interest rates begin a cycle of normalization, these banks are well-positioned to maintain margins while benefiting from a shift toward private sector credit expansion.

Industrial Outlook: Cement and Steel

The construction-aligned sectors, specifically Cement and Steel, are also flashing buy signals. Lucky Cement, the sector leader, maintains a “BUY” stance with a target price of 731 PkR. The broader cement cluster, including DG Khan Cement and Maple Leaf, shows a trend of improving price-to-earnings (PE) multiples as we look toward FY27E, indicating an expectation of a construction rebound. In the steel sector, Mughal Iron & Steel and International Steels (ISL) both offer significant upside, with ISL’s target price of 151 PkR sitting comfortably above its current 90 PkR mark.

While the majority of the coverage is bullish, the report maintains objectivity by identifying outliers. The Hub Power Company (HUBC) and Engro Polymer & Chemicals (EPCL) are notable exceptions with “SELL” ratings, reminding investors that sector-specific challenges, such as contract renegotiations or global commodity price shifts, require a selective approach even in a bull market.

Disclaimer: This report is for informational purposes and does not necessarily reflect the views of ‘Money Matters Pakistan’. We welcome any corrections or alternative viewpoints from our readers to ensure a balanced perspective.