First sovereign Eurobond in four years marks a historic comeback; yield drops below 7% amid strong investor appetite.

Key Takeaways

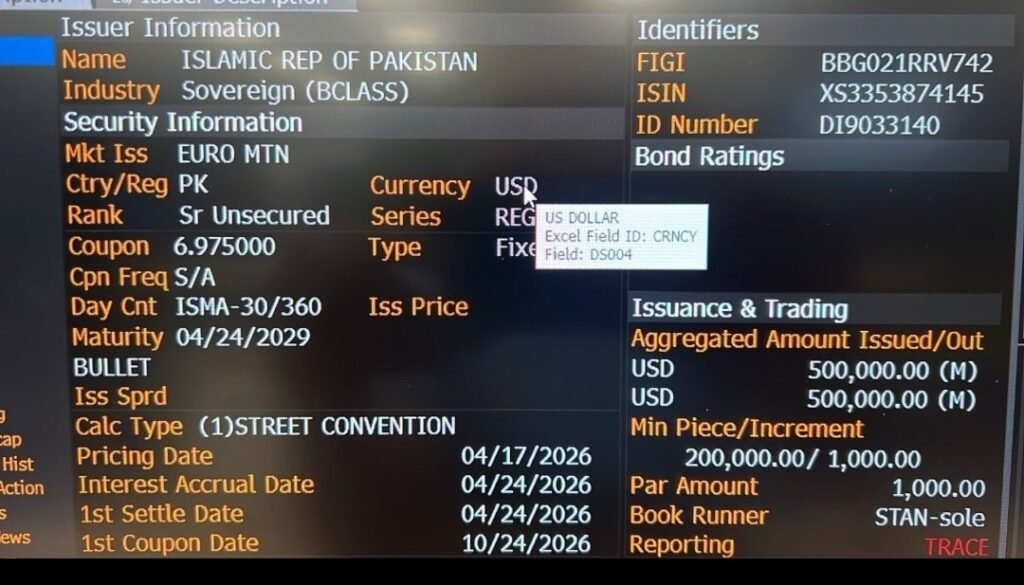

• Market Re-entry: Pakistan issued its first Eurobond in four years, raising $500M with a maturity date in April 2029.

• Investor Confidence: The bond was priced at an attractive 6.95%, reflecting an upgraded global perception of Pakistan’s credit.

• Debt Cycle Management: The issuance follows the successful repayment of $1.43B in external debt earlier this month.

Karachi, Pakistan – In a landmark moment for the national economy, Pakistan has successfully returned to the international capital markets after a four-year hiatus. On Friday, April 17, 2026, the government issued a $500 million three-year Eurobond, marking the first time Islamabad has tapped into global commercial borrowing since 2022. A news story published by Arab News confirms the transaction was completed under the government’s Global Medium-Term Note (GMTN) Program.

The issuance was priced at a surprisingly competitive interest rate of 6.95%. This sub-7% yield is being hailed by financial experts as a strong vote of confidence from international investors, especially given the current global geopolitical tensions and high interest rate environment. Khurram Schehzad, Adviser to the Finance Ministry, confirmed the success on 𝕏, noting that the bond attracted robust demand and effectively matures in April 2029.

Returning to the Eurobond market isn’t just about the $500 million; it’s about reclaiming our seat at the global financial table.

This re-entry follows a week of high-stakes financial maneuvering. Just days prior, on April 8, Pakistan successfully repaid a $1.3 billion Eurobond, which officials termed a “non-event” that proved the country’s debt management capacity. The new $500 million issuance, coming on the heels of $2 billion in bilateral assistance from Saudi Arabia, has further bolstered foreign exchange reserves, which currently stand at a healthy $20.52 billion.

A sub-7% yield in today’s volatile climate is a clear signal that the world is betting on Pakistan’s economic recovery.

According to a report by Mettis Global, this move is part of a broader strategy by Finance Minister Muhammad Aurangzeb to diversify funding sources. The successful Eurobond sale sets a positive precedent for upcoming initiatives, including the potential launch of “Panda Bonds” in the Chinese market later this year.