Pakistan’s 2018 crypto ban officially replaced.

Key Takeaways:

- State Bank of Pakistan’s BPRD Circular No. 10 of 2026 replaces the 2018 ban, allowing banks to open accounts for PVARA-licensed crypto firms under strict AML rules.

- Client Money Accounts must be PKR-denominated, strictly segregated, and cannot be used as collateral or for financing.

- Banks are barred from investing, trading, or holding virtual assets using their own funds or customer deposits.

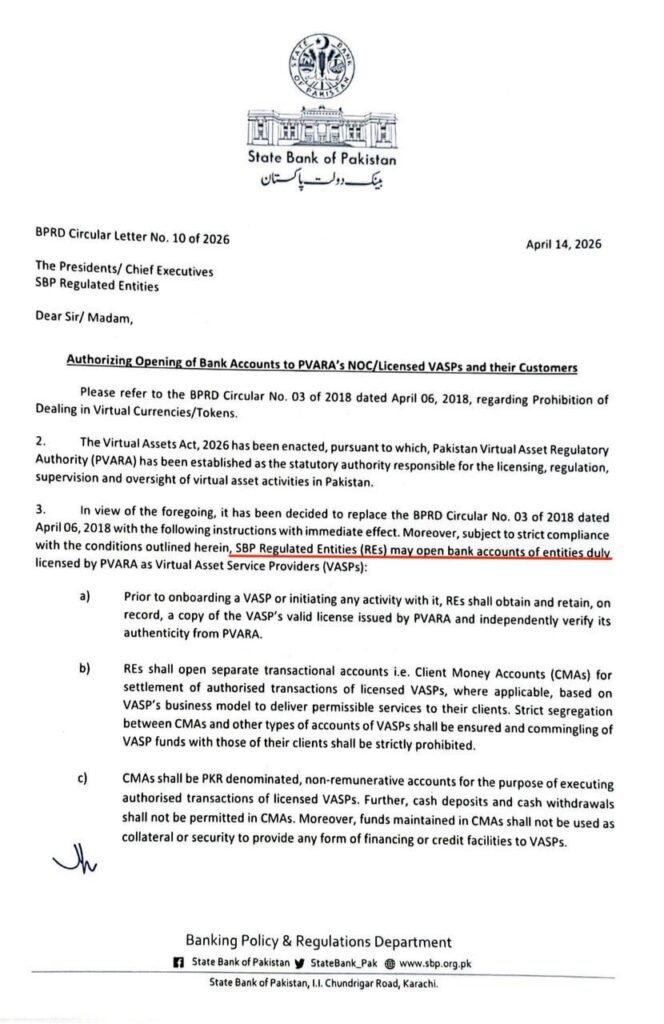

Islamabad, Pakistan – For eight years, a single State Bank of Pakistan circular kept the country’s banking system firmly shut to cryptocurrency businesses. That changed on April 14, 2026. The SBP has issued BPRD Circular Letter No. 10 of 2026, formally replacing the 2018 prohibition and allowing regulated banks to open and maintain accounts for Virtual Asset Service Providers licensed by the Pakistan Virtual Assets Regulatory Authority.

The circular, issued by the Banking Policy and Regulations Department states directly that the Virtual Assets Act, 2026 has been enacted, pursuant to which PVARA has been established as the statutory authority responsible for the licensing, regulation, supervision and oversight of virtual asset activities in Pakistan. The circular formally replaces BPRD Circular No. 03 of 2018 dated April 6, 2018, which had prohibited all banks, DFIs, microfinance banks, and payment system operators from processing, dealing in, or facilitating transactions related to virtual currencies.

A single page from the State Bank of Pakistan has done what years of informal crypto activity could not: given Pakistan’s digital asset sector a legitimate banking address.

What Banks Can and Cannot Do

The circular sets out clear conditions. Banks must first obtain and independently verify a copy of the PVARA license before onboarding any Virtual Asset Service Provider. They are required to open separate Client Money Accounts for the settlement of authorised transactions, with strict segregation between those accounts and all other VASP funds. The commingling of VASP funds with client funds is explicitly prohibited.

Client Money Accounts must be PKR-denominated and non-remunerative. Cash deposits and cash withdrawals are not permitted in these accounts, and funds held in them cannot be used as collateral or to provide any form of financing or credit to VASPs.

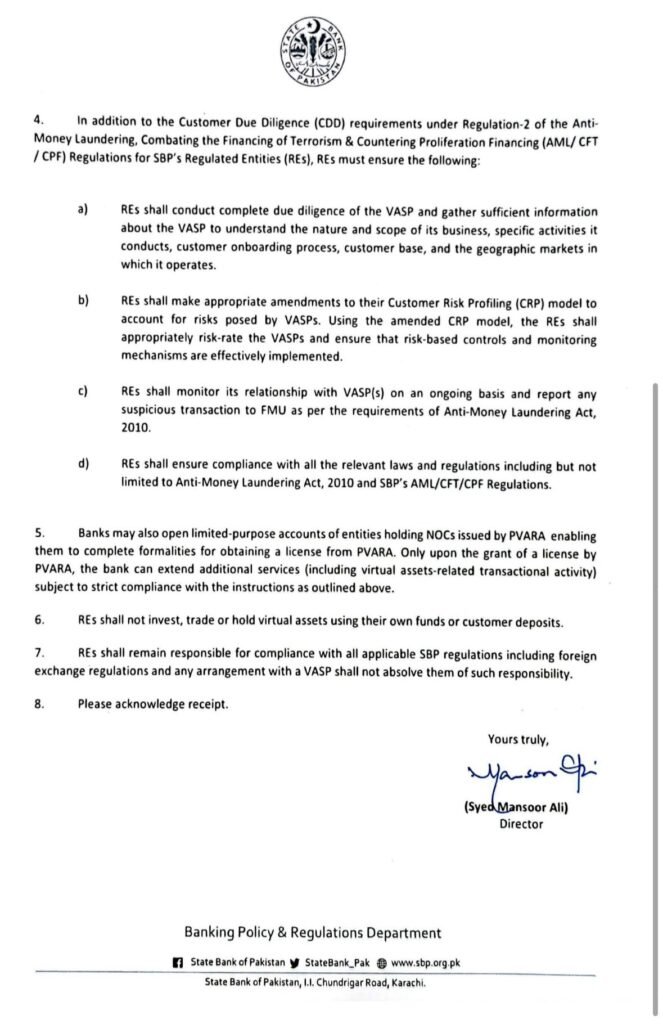

The circular also specifies that banks may open limited-purpose accounts for entities holding NOCs from PVARA, enabling them to complete the formalities for obtaining a full license. Only after a full license is granted can banks extend additional services including virtual asset-related transactional activity.

Critically, the circular states that regulated entities shall not invest, trade, or hold virtual assets using their own funds or customer deposits, a firm boundary keeping banks as facilitators rather than participants in the digital asset market.

The AML Framework Banks Must Follow

The circular imposes comprehensive Anti-Money Laundering and Countering Financing of Terrorism obligations. Banks must conduct complete due diligence on each VASP, update their Customer Risk Profiling models to account for risks specific to virtual asset businesses, monitor VASP relationships on an ongoing basis, and report suspicious transactions to the Financial Monitoring Unit under the Anti-Money Laundering Act, 2010. Banks also remain fully responsible for compliance with all applicable SBP regulations, including foreign exchange regulations, and no arrangement with a VASP can absolve them of that responsibility.

The Broader Context

This circular is the direct operational output of the Virtual Assets Act, 2026, which Pakistan’s parliament passed in early March of this year. The Block reported that the legislation converts PVARA into a permanent federal body with the power to license and supervise crypto service providers, and introduces criminal penalties for unlicensed operations including fines of up to PKR 50 million and imprisonment of up to five years.

Pakistan has an estimated 30 to 40 million crypto users. Until today, none of that activity had a legitimate banking home. The SBP circular changes that, one regulated account at a time.

Business Recorder reported that PVARA had already been discussing the withdrawal of the 2018 SBP circular since its first board meeting in August 2025, with PVARA Chairman Bilal bin Saqib stating that PVARA will safeguard financial integrity while fostering innovation, investment, and opportunity in the virtual assets space, with the goal of building trust domestically and enhancing Pakistan’s credibility as a forward-thinking player in the global virtual assets economy.

The Express Tribune had earlier reported that Finance Minister Muhammad Aurangzeb warned that Pakistan risks slipping back onto the grey list of the Financial Action Task Force due to unregulated digital transactions being carried out by roughly 15 per cent of the population.

PVARA has already issued No-Objection Certificates to global exchanges including Binance and HTX. The April 14 circular now gives those exchanges and others working toward full PVARA licenses a clear path to open the bank accounts they need to operate within Pakistan’s formal financial system.