AKD Research expects higher offtakes and dividends at FFC and EFERT, as FATIMA’s profits fall on weak demand and cost pressures

Key Takeaways

- Sector profitability improving: AKD Research expects the fertilizer universe’s profitability to rise about 5% YoY in 1QCY26, driven mainly by higher offtakes at FFC and EFERT, although margin compression from phosphate‑mix and higher input costs will cap the upside.

- FFC and EFERT as earnings and dividend leaders: FFC’s net profit is projected to jump 34% YoY, with EFERT up 10%, both supported by stronger Urea and DAP sales and higher other income, while dividend per share (DPS) is expected to rise at both companies.

- FATIMA under pressure: FATIMA’s profitability is forecast to plunge 41% YoY on weaker offtakes, a less favorable product mix, and lower yields/equity‑related income, highlighting rising company‑level risks in an otherwise solid sector.

Karachi, Pakistan – Pakistan’s listed fertilizer sector is poised for modest earnings growth in the first quarter of CY26, with FFC and EFERT leading the performance band while FATIMA faces a sharp profitability setback, according to AKD Research’s 1QCY26 result‑preview note released on April 18, 2026.

Sector‑wide outlook

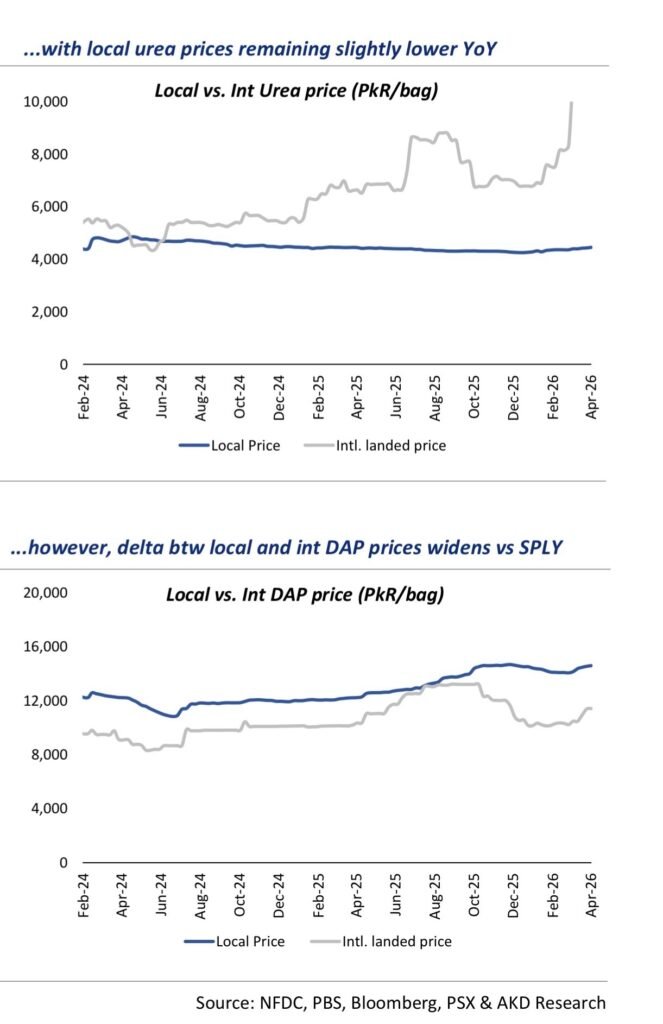

AKD’s fertilizer universe is projected to post a 5% YoY rise in profitability for 1QCY26, underpinned by stronger offtakes at FFC and EFERT that are expected to push total sales up 26% YoY to PkR184.3 billion. Gross margins, however, are forecast to contract sharply by 7.3 percentage points to 29.9% from 37.2% in the same‑period last year, mainly due to a higher share of phosphate nutrients in the sales mix and cheaper core‑marginal products as phosphoric‑acid prices rise. Other income is expected to grow 24% YoY, largely on higher dividend receipts, while finance costs are seen climbing on increased net borrowings, keeping the decremental impact of margins partially offset by stronger top‑line and financial‑income growth.

FFC: volume and dividends in focus

FFC is expected to post the strongest earnings growth in the group, with net profit forecast to rise 34% YoY to PkR17.8 billion (EPS PkR12.5) versus PkR13.3 billion (EPS PkR9.3) a year ago. The jump is driven by a 12% YoY rise in Urea offtakes and a 2.1x increase in DAP volumes, alongside a 33% YoY rise in other income, chiefly from dividends of energy‑related subsidiaries and associates such as FWE I, II, and TEL. Gross margins are nevertheless expected to ease to 29.0% from 35.6% in the prior‑year quarter due to a higher proportion of DAMP in the offtake mix, while finance costs are projected to climb 26% YoY to PkR2.1 billion on higher borrowings. AKD anticipates FFC to announce an interim dividend of PkR9.0 per share, reflecting the management’s continued commitment to shareholder returns.

EFERT: solid growth amid margin pressure

EFERT is expected to post a more moderate but still positive 10% YoY growth in net profit to PkR3.2 billion (EPS PkR2.4) versus PkR2.9 billion (EPS PkR2.2) in 1QCY25. Sales are projected to rise 22% YoY, supported by 7% and 64% YoY growth in Urea and DAP offtakes, respectively, even as gross margins are forecast to fall 4.7 percentage points to 30.5% due to a lower share of higher‑margin Urea in the sales basket. Other income is expected to nearly double 2.1x YoY on higher short‑term investments, while finance costs are also projected to double as borrowing increases to meet higher working‑capital needs led by elevated inventory levels and capital‑expenditure related to the Pressure Enhancement Facility project. AKD expects EFERT to distribute a dividend of PkR2.5 per share, aligning payout with earnings growth.

FATIMA’s profit slide amid weak demand

FATIMA, on the other hand, faces a tough first quarter, with profitability projected to contract by 41% YoY to PkR4.9 billion (EPS PkR2.3) from PkR8.4 billion (EPS PkR4.0) in 1QCY25. Revenue is expected to fall 17% YoY, on the back of a steep 59% drop in Urea offtakes and a 30% decline in CAN, only partially offset by a 30% increase in NP sales. Margins are also forecast to shrink to 31.4% from 40.4%, hit by weaker offtakes, a heavier load of phosphate products, and a lower share of output from the base plant that benefits from relatively cheaper gas prices. Other income is projected to fall 16% YoY due to lower yields and equity‑market correction during the quarter, further denting bottom‑line performance.

The jump is driven by a 12% YoY rise in Urea offtakes and a 2.1x increase in DAP volumes, alongside a 33% YoY rise in other income, chiefly from dividends of energy‑related subsidiaries and associates such as FWE I, II, and TEL.

Sector valuation and investment view

AKD Research maintains an overweight stance on the fertilizer sector, citing stable demand, resilient earnings, and strong cash flows that translate into attractive dividend yields for investors. The brokerage keeps a ‘BUY’ rating on FFC and ENGROH, with December 2026 target prices of PkR801 and PkR351 per share, respectively, implying single‑digit P/E multiples and dividend yields in the mid‑single‑digit to high‑single‑digit range. EFERT and FATIMA are also rated ‘BUY’, supported by their relatively low P/E levels and dividend yields above 6%, though AKD’s base‑case model prices must factor in the near‑term volatility in FATIMA’s earnings and gas‑cost trajectory.

Overall, the 1QCY26 preview underscores that Pakistan’s fertilizer sector remains a core income‑oriented play for domestic investors, with FFC and EFERT looking best positioned to benefit from volume recovery and solid dividend policies, while FATIMA’s performance will hinge on any improvement in demand and a more favorable energy‑cost environment.