Record Panda issuances and a 260-basis-point yield gap are driving a historic shift in how the world’s biggest borrowers fund themselves

Key Takeaways

•Panda bond issuance tripled to 27.8 billion yuan in March 2026 alone, driven by a 260bps yield advantage over U.S. Treasuries.

•The U.S. dollar’s reserve share has hit a 30-year low.

•And the yuan’s expanding role in commodity trade, formalized at Hormuz, suggests the shift extends well beyond bond markets.

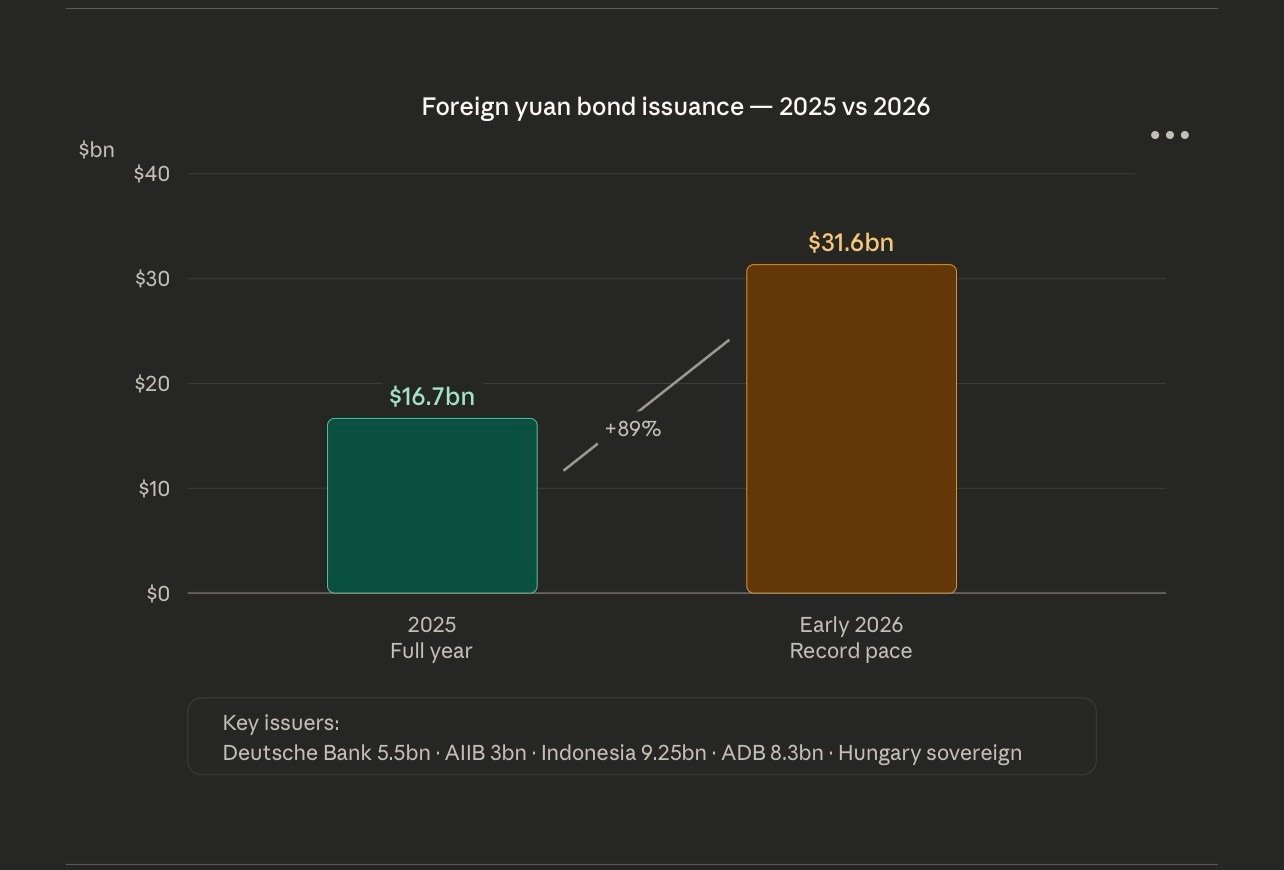

Money Matters Monitoring — The world’s largest banks, governments, and multilateral lenders are accelerating a structural shift away from dollar-denominated debt, with foreign Panda bond issuance tripling year-on-year to 27.8 billion yuan in March 2026 alone. Longbridge Financial reported that total yuan-denominated financing by foreign borrowers hit a record 218 billion yuan ($31.6 billion) in early 2026 — already eclipsing 2025’s full-year figure.

The arithmetic driving the trend is blunt. Trading Economics data shows China’s 10-year government bond yield sitting at 1.82%, against the U.S. Treasury’s 4.46% — a spread of 260 basis points, the widest since August 2025. For large institutional borrowers, that differential translates into meaningfully lower interest costs, and the market is responding.

China Daily reported that Deutsche Bank priced the largest-ever foreign bank Panda bond at 5.5 billion yuan in March 2026, oversubscribed 1.55x on its 3-year tranche and 1.63x on its 5-year. Xinhua noted that the Asian Infrastructure Investment Bank raised 3 billion yuan the same month, with the AIIB confirming that 58% was absorbed by overseas investors — a record demand figure for the institution. Bastille Post reported that Indonesia priced 9.25 billion yuan of sovereign bonds a full percentage point below its equivalent euro issuance, a stark illustration of the cost advantage now available in Chinese capital markets. The Asian Development Bank, Morgan Stanley, Barclays, and Hungary have all returned to the Panda market as repeat issuers, with MEXC News reporting the ADB alone raised 8.3 billion yuan in early 2025.

The macro backdrop reinforces the momentum. BestBrokers data shows the U.S. dollar’s share of global currency reserves has fallen to 56.32%, its lowest since 1995, while Trading Economics noted that China’s holdings of U.S. Treasuries have dropped to approximately $683 billion after nine consecutive months of sales. NBER research found the U.S. Treasury convenience yield had turned negative at -0.25% for 10-year paper — a striking reversal of the safe-haven premium that long underpinned dollar dominance. FXC Intelligence reported that the yuan now settles 34.5% of China’s cross-border trade, with outbound settlements reaching 53.9% in 2025, while the Global Times noted that China’s dim sum bond market hit a record 870 billion yuan last year.

Beyond bonds, the de-dollarisation dynamic is extending into commodity trade. CryptoRank reported that Iran’s $1-per-barrel Strait of Hormuz toll — payable in yuan or Bitcoin — carries the force of law, with pre-ceasefire payments already processed in RMB. The BBC confirmed a U.S.-Iran ceasefire has reopened the strait, but the yuan-denominated toll structure remains in place, codifying RMB pricing in one of the world’s most strategically sensitive energy corridors.

The combined picture is one of a borrowing environment in structural transition. The question for multinationals, sovereigns, and development banks is no longer whether RMB financing is competitive — at 260 basis points cheaper than dollar debt, it plainly is. The question is how quickly they can access it, and whether China’s capital markets can absorb the scale of demand now heading their way.